RBA Cash Rate Increase Mortgage Repayments: What the 4.35% Decision Means for You

If you're on a variable-rate home loan right now, today's RBA decision is going to sting. For the third time in 2026, the Reserve Bank of Australia has lifted the cash rate by 25 basis points, pushing it back to 4.35%, the same peak reached in 2024 and the highest level since December 2011. The question most mortgage holders are asking isn't just "how much does this cost me?" It's "what do I actually do about it?"

The team at Osinski Finance, a family-owned mortgage brokerage based in Rockingham, WA, with 25 years of combined banking and finance experience, has put together this breakdown to help you understand exactly how RBA cash rate increases affect mortgage repayments and what options you have right now.

Quick Answer: How Does Cash Rate Affect Home Loans?

The RBA cash rate increase to 4.35% will likely raise variable rate home loan repayments within weeks. Most lenders pass on the full 25 basis point rise, which translates to roughly $77 more per month on a $500,000 loan, $115 on a $750,000 loan, and $154 on a $1 million loan. If you're on a fixed-rate mortgage, your repayments won't change until your fixed period ends, but if that expiry is coming up, now is the time to plan. For borrowers already stretched by the two earlier hikes this year, it's worth reviewing your loan options sooner rather than later.

Why Did the RBA Raise the Cash Rate Again?

The RBA's Monetary Policy Board pointed to the conflict in the Middle East as a key driver, noting it had produced sharply higher fuel and commodity prices that were already adding to inflation. The Board flagged that many businesses facing rising costs were beginning to pass them on to consumers and that short-term inflation expectations had also moved higher.

This RBA monetary policy decision brings the cash rate back in line with the 2024 peak of 4.35%. While that peak was ultimately temporary, the speed at which the rate has climbed again in 2026, three hikes across three meetings, has caught many borrowers off guard. If you have been wondering how does cash rate affect your home loan in practical terms, the sections below break it down by loan size.

If you want to track where the rate goes from here, bookmark the Osinski Finance Interest Rate Tracker for ongoing updates.

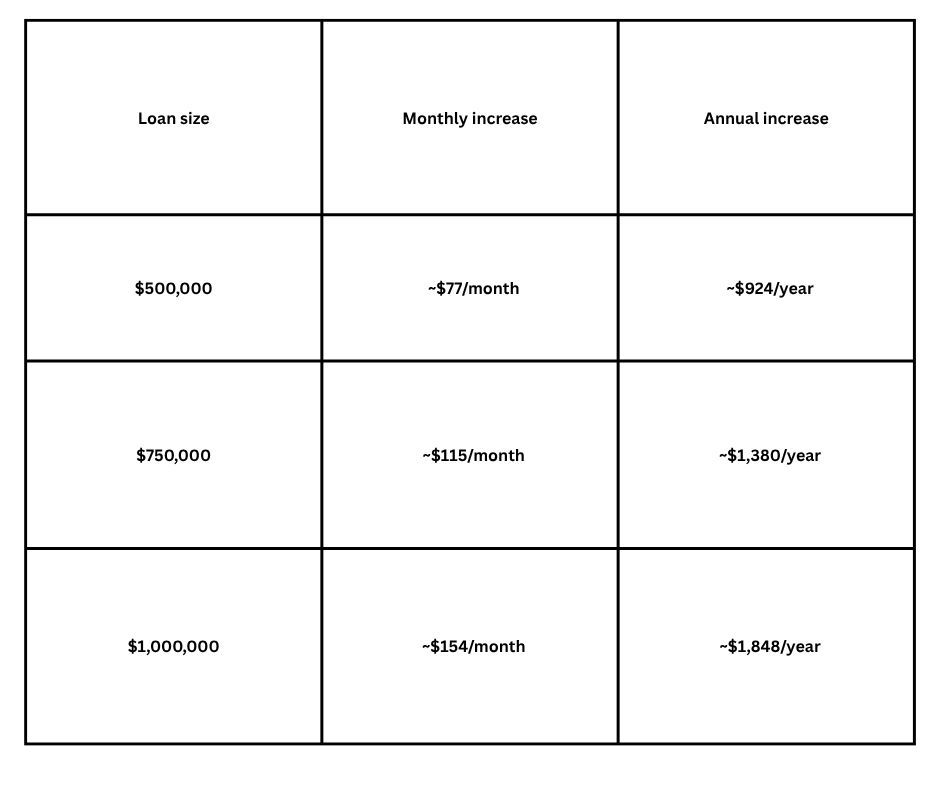

What Does This Mean for Your Monthly Mortgage Repayments?

Understanding how an RBA cash rate increase mortgage repayments starts here. Unless you are locked in on a fixed-rate mortgage, your lender will almost certainly follow the RBA's lead and raise the interest rate on your variable rate home loan within the next few weeks.

Here is a straightforward look at how the 25 basis point rise affects monthly repayments for an owner-occupier paying principal and interest on a 25-year loan:

These figures assume your lender passes on the full 25 basis points. Some lenders may vary.

What if you're on a fixed rate?

If you are currently on a fixed-rate mortgage, today's hike will not affect your repayments until your fixed term expires. However, if your fixed period is due to end in the next six to twelve months, this is exactly the right time to start reviewing your options. Rolling onto a variable rate without a strategy in this environment could mean a significant jump in your monthly costs.

For a detailed look at how fixed and variable products compare right now, read our post on fixed-rate vs variable home loan rates.

One thing that may soften the blow

There is a small silver lining worth understanding. When the cash rate fell from the previous 4.35% peak, many lenders kept borrowers on the same monthly repayment amount rather than reducing it. In practice, this meant borrowers were paying down more principal each month rather than interest.

If that applies to your loan, this latest rate hike may not change the dollar amount you physically pay each month. What it does change is how your repayment is split: a greater portion will now go toward interest rather than reducing your principal balance.

To know for certain what your lender is doing with your specific loan, get in touch with us in the coming days once the banks have confirmed their position.

What Are Your Options Now?

The third RBA rate hike of the year is another tough pill for variable rate borrowers, but there are genuinely useful steps available depending on your situation.

Review your home loan rate

If it has been more than 12 months since your last home loan review, this is a strong prompt to act. The lending landscape shifts constantly and there is a real chance a lower-rate product exists in the market right now that your lender has no incentive to tell you about.

A straightforward rate review could reveal whether you can access a more competitive deal, either with your existing lender or a new one.

Refinance to a better deal

When a rate hike hits, one of the most effective moves for Australian borrowers is to refinance their home loan to a lender offering a lower rate. With access to nearly 100 lenders, the team at Osinski Finance can quickly identify whether a better option is available for your circumstances and borrowing profile.

Even a 0.25% to 0.50% reduction in your interest rate can produce meaningful savings across the life of your loan.

Renegotiate with your current lender

Many borrowers do not realise their existing lender may be willing to negotiate. Presenting a genuine refinance alternative as leverage can prompt your bank to offer a sharper rate without the cost and effort of switching. This is a conversation a broker can run on your behalf.

Switch to interest-only for a short period

For borrowers experiencing temporary financial pressure, moving to an interest-only home loan for a defined period can reduce your monthly commitments while you stabilise. This is not a long-term strategy, but as a short-term pressure valve, it is worth understanding properly before dismissing.

Explore debt consolidation

If you are carrying other debts alongside your mortgage, debt consolidation through your home loan can lower your overall monthly obligations. Rolling higher-interest debts into your mortgage typically reduces your total monthly outgoings, freeing up cash flow during a period of rising costs.

Every household's situation is different. The right move for your neighbour may not be the right move for you.

Key Takeaways

- The RBA lifted the cash rate to 4.35% on this decision, its third increase in 2026 and the highest rate since December 2011.

- Variable rate home loan repayments will likely increase within weeks of this decision, once lenders pass on the rise.

- A $500,000 loan faces roughly $77 more per month; a $750,000 loan around $115; a $1 million loan approximately $154.

- If you have not had a home loan review in the past year, now is an ideal time to check whether a better rate is available.

- Options available to stretched borrowers include refinancing, renegotiating with your current lender, switching to interest-only temporarily, or consolidating debts.

- Borrowers on fixed rates are insulated now, but those approaching the end of a fixed term should plan for the transition.

Considering Your Options? Talk to Osinski Finance

Whether you need help with a home loan, are investing in a property, or want to refinance your home loan, Osinski Finance can help you compare your options and find a loan that suits your situation.

Ready to review your next step? Contact us today for a no-obligation chat.

Frequently Asked Questions

How does the RBA cash rate increase affect my mortgage repayments?

RBA cash rate increases mortgage repayments by prompting most variable rate lenders to raise the interest rate on home loans in kind. This means the interest portion of your monthly repayment goes up, increasing the total amount you owe each month. For a principal and interest loan of $500,000 over 25 years, a 0.25% rate rise adds approximately $77 to your monthly repayment. The exact impact depends on your loan size, remaining term, and whether your lender passes on the full increase. If you are unsure how the change affects your specific loan, your lender or a mortgage broker can run the numbers for you.

Will my fixed-rate home loan be affected by this rate rise?

No, your repayments will not change while you remain within your fixed-rate period. A fixed-rate mortgage locks in your interest rate for the agreed term, regardless of what the RBA does in the meantime. However, once your fixed period ends and you roll onto a variable rate, the prevailing rate at that time will apply. If your fixed term is expiring within the next six to twelve months, it is worth reviewing your options now so you are not caught off guard by the transition.

What is the difference between a fixed and variable rate home loan in this environment?

Understanding how does cash rate affect home loans depends partly on which type of loan you hold. A fixed-rate home loan locks your interest rate for a set period, typically one to five years, giving you certainty over your repayments regardless of rate movements. A variable rate home loan fluctuates with the market and is directly influenced by RBA decisions. In a rising-rate environment, fixed rates offer payment stability. In a falling rate environment, variable rates allow you to benefit from reductions sooner. The right choice depends on your financial situation, risk tolerance, and outlook for rates, which is why speaking with a broker before making the switch is worthwhile.

Should I refinance my home loan because of this rate rise?

For many Australian borrowers, the decision to refinance a home loan after a rate hike comes down to one question: Is your current rate still competitive? If it has been 12 months or more since you last reviewed your rate, there is a reasonable chance a better product exists in the market. Refinancing typically involves some upfront costs, so a broker can help you calculate whether the long-term savings outweigh the switching costs for your specific situation. Not every borrower will benefit from refinancing, but many will, and it costs nothing to find out.

Can I negotiate a better rate with my existing lender?

Yes, in many cases, lenders will negotiate rather than lose a customer to a competitor. If you can demonstrate that you have found a lower rate elsewhere, your current lender may match or beat it. The success of this approach depends on your loan size, credit history, and repayment history. A mortgage broker can run this negotiation on your behalf, using their lender relationships and market knowledge to give you the best possible outcome.

What is an interest-only home loan, and is it right for me?

An interest-only home loan allows you to pay only the interest portion of your loan for a set period, typically one to five years, rather than both principal and interest. This lowers your monthly repayments during the interest-only period but does not reduce your loan balance. It can provide short-term cash flow relief during a period of financial pressure, but the full principal and interest repayments will be higher once the interest-only period ends. It is not suitable for everyone, and the long-term cost implications are worth understanding before proceeding.

What is debt consolidation, and how can it help with rising repayments?

Debt consolidation involves rolling multiple debts, such as credit cards, personal loans, or car loans, into your home loan. Because home loan interest rates are typically much lower than other forms of debt, this can significantly reduce your overall monthly repayment obligations. The trade-off is that you extend the repayment period for those debts and may pay more interest over time. For borrowers under short-term financial pressure from rate rises, it can be a useful tool, but it is best explored with a broker who can model the full picture for your circumstances.

How many times has the RBA raised the cash rate in 2026?

As of this decision, the RBA has raised the cash rate three times in 2026, with each increase being 0.25%. This has brought the rate from 3.85% back up to 4.35%, matching the 2024 peak. The RBA has cited rising inflation pressures, including higher fuel and commodity prices linked to the Middle East conflict, as the primary drivers of this tightening cycle. For ongoing updates on the cash rate, you can track movements via the Osinski Finance Interest Rate Tracker.

How long does it take for a rate rise to affect my home loan repayments?

Most lenders announce their response to an RBA decision within a few days and implement the new rate within two to four weeks. Some lenders move faster. Once the new rate takes effect, your next monthly repayment will reflect the change. If you are unsure of the timeline for your specific lender, check your online banking or contact them directly for confirmation. For a deeper explanation of the mechanics, read our post on how long it takes for a rate rise to kick in.

What should I do right now if I am struggling with my mortgage repayments?

The first step is to get a clear picture of your current loan compared to what is available in the market. Contact your lender to ask about hardship provisions, rate reductions, or switching options. Speak with a mortgage broker to understand whether refinancing or restructuring your loan could reduce your monthly costs. Do not wait until you are in default. Lenders and brokers have more tools available to help borrowers who engage early. The Osinski Finance team offers obligation-free consultations and can be reached on (08) 9511 1177 or at firststep@osinski.com.au.

Updates